The Bank Bailout Trap

The government has already paid more than 80,000 crore taka and will have to pay another 100,000 crore taka in the future to maintain the Sammilito Islami Bank under the Bank Resolution Ordinance.

Zia Hassan

The public discourse around the newly legislated Bank Resolution Act, particularly the Section 18(a), appears to be a gross simplification of a highly complex issue.

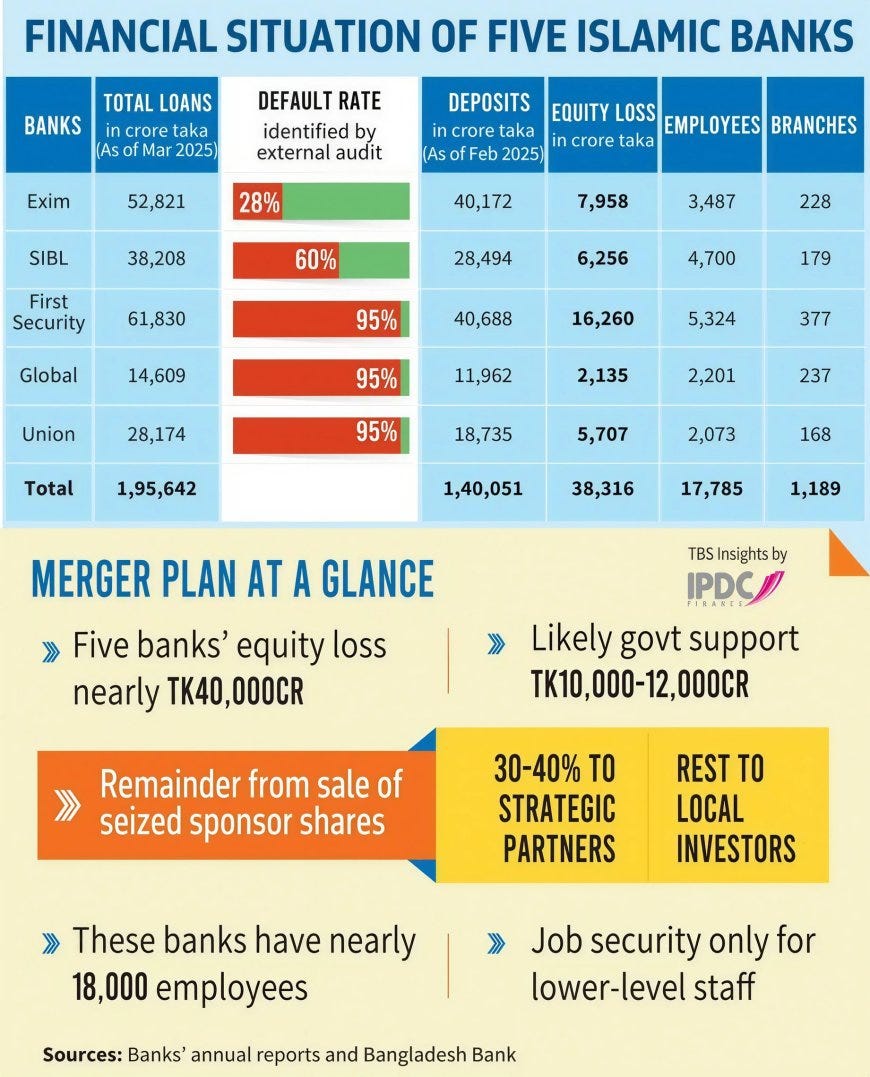

According to public perception, the new act allows the return of the Sammilito Islami Bank -- formed by merging five weak banks through the Banking Resolution Ordinance of the interim administration -- to its old owners, especially to S Alam.

Sheikh Hasina’s cashier S Alam has looted nearly Tk 100,000 crore from the banking sector. Returning the looted banks to S Alam would be as immoral and preposterous as marrying the rape victim to the rapist. This mechanism would be contrary to restoring discipline in the banking sector.

However, the idea that the amendment made to Section 18(a) of the Banking Resolution Bill 2026 was specifically brought to bring back S Alam is misinformed.

This is a highly nuanced and complex issue.

A contrarian perspective is that, ignoring the advice of the World Bank and many economists, the previous governor of the central bank effectively nationalized the bankrupt banks and shifted the burden of the bank looting that occurred during the Hasina regime onto the people of Bangladesh through the public finances.

To protect the public purse from this, some critical corrections were needed in this ordinance, because the Sammlito Islami Bank is creating a very big problem that no one is talking about.

The conventional wisdom is that the bravest step taken by the interim government to restore discipline in the banking sector was the Banking Resolution Ordinance 2025 -- merging five banks and removing ownership from the sponsor directors responsible for destroying them.

As a result, when converting this ordinance into a law, the provision that allows old shareholders to regain ownership by paying 7.5% of the state’s invested money upfront and the remaining 92.5% within two years is being portrayed as something that S Alam will definitely use. The problem is that this narrative is only a fraction of the story.

These five banks are all bankrupt. The net asset value of the banks is negative and the accounting equity is zero. That is, the liabilities of these banks exceed their assets. So when the previous governor merged these five banks and created Bangladesh’s first state-owned Islamic bank, he essentially nationalized some bankrupt banks. Through this, he shifted the burden of repaying 142,000 crore taka in deposits belonging to 7.5 million depositors of these looted banks onto the state.

Against this 142,000 crore taka in deposits, there are 193,000 crore taka in loans outstanding, 90% of which are now non-performing. Without recovering these loans, 35,000 crore taka was required from the public coffers in the interim period alone to repay this 142,000 crore, and in the future, the people will have to pay more than 100,000 crore taka.

And my reading is that the government does not want that; the government wants to sell the banks and keep the door open for the old shareholders in that process. That is the essence of the amendment made to the Banking Resolution Bill 2026.

Yes, theoretically, this has paved the way for S Alam or Nazrul Islam to return. But that is only one part of the story, and arguably not even the main part.